Audit of management practices of missions - Jakarta

March 2018

Table of Contents

Executive summary

Global Affairs Canada manages Canada’s International Platform Branch — a global network of 179 Missions in 109 countries that supports the international work of Global Affairs Canada and 37 partner departments, agencies and co-locators.Footnote 1 Administrative activities that support the Department’s Missions require effective and efficient management practices to help ensure sound stewardship of resources.

Rationale for this audit

In 2015, the Department initiated an internal investigation into the Canadian Embassy in Haiti, and found that fraudulent schemes had been put in place by locally engaged staff that resulted in estimated government losses of $1.7 million. Given the findings in Haiti, the Deputy Minister of Foreign Affairs requested a series of management practice audits of selected Missions to determine whether similar issues could be taking place at other Canadian Missions abroad.

The Office of the Chief Audit Executive conducted a risk assessment to identify those Missions susceptible to higher levels of fraud risk and therefore selected for audit. A first phase of Mission audits was initiated in 2016-17. As part of a second phase initiated in 2017-18, the Jakarta Mission was one of five Missions operating in a higher fraud risk environment selected for audit.

What was examined

The objective of this audit was to provide assurance that sound management practices and effective controls are in place to ensure good stewardship of resources at the Jakarta Mission to support the achievement of Global Affairs Canada objectives. This audit examined the Mission’s management practices related to the Management and Consular Services Program with regard to oversight and monitoring, procurement and asset management, and human resources between April 2014 and September 2017.

What was found

The audit team found that some processes established by Headquarters related to planning, monitoring, procurement, asset management (including property, vehicle fleet, inventory, and revenues), and human resources were not consistently followed, and some key controls were not in place or were not followed. As a result, there is an absence of some Mission-generated, reliable information for decision-making to promote and demonstrate sound stewardship of resources.

The audit team found that the Mission does not have strong planning and monitoring processes in place over finance, procurement, and asset management. Concerns were noted in regard to the management of assets at the Mission, specifically the monitoring and management of recreational facilities, inventory, leased properties, vehicles, and consular revenues. Further, the auditors found gaps in the management of procurement processes, including issues with the selected method of procuring, the initiation and management of contracting processes, the achievement of value for money, and compliance with procurement policies. Lastly, the audit team found that staffing file documentation was missing or incomplete, and one staffing process was improperly managed.

Conclusion

The audit concluded that there were significant weaknesses in the management practices and controls in place to ensure sound stewardship of resources at the Jakarta Mission. There is a lack of management oversight and monitoring in the areas of local procurement, asset management, consular revenue and inventory management. The Mission does not leverage available information to support decision-making and to promote good stewardship of resources. Processes established by Headquarters relating to finance, procurement, contracting and human resources are not consistently followed and some key controls are not in place or not being followed.

[REDACTED]

The audit team verbally debriefed the HOM and the MCO after completion of work on-site. As a result, mission management has immediately taken many corrective measures to address issues identified by the audit.

Recommendations are detailed in Section 5 of this report.

Statement of Conformance

In my professional judgment as Chief Audit Executive, this audit was conducted in conformance with the Institute of Internal Auditors' International Standards for the Professional Practice of Internal Auditing and with the Treasury Board Policy and Directive on Internal Audit, as supported by the results of the quality assurance and improvement program. Sufficient and appropriate audit procedures were conducted, and evidence gathered, to support the accuracy of the findings and conclusion in this report, and to provide an audit level of assurance. The findings and conclusion are based on a comparison of the conditions, as they existed at the time, against pre-established audit criteria that were agreed upon with management and are only applicable to the entity examined and for the scope and time period covered by the audit.

Brahim Achtoutal

Chief Audit Executive

Date

1. Background

Global Affairs Canada (the Department) manages Canada’s diplomatic and consular relations, promotes international trade and leads Canada’s international development and humanitarian assistance programs. It also manages Canada’s International Platform Branch — a global network of 179 Missions in 109 countries that supports the international work of Global Affairs Canada and 37 partner departments, agencies and co-locators.Footnote 2 According to the 2016-17 Global Affairs Canada Departmental Results Report, $931M was spent to operate and support the Missions. Administrative activities that support the Department’s Missions require effective and efficient management practices to help ensure sound stewardship of resources.

In 2015, the Department initiated an internal investigation into the Canadian Embassy in Haiti, and found that fraudulent schemes had been put in place by locally engaged staff that resulted in estimated government losses of $1.7 million. Given the findings in Haiti, the Deputy Minister of Foreign Affairs requested a series of management practice audits of selected Missions to determine whether similar issues could be taking place at other Canadian embassies abroad.

The Office of the Chief Audit Executive conducted a risk assessment to identify those Missions susceptible to higher levels of fraud risk and therefore selected for audit. The following factors were considered:

- complexity of the Mission in terms of the number and kinds of services provided;

- size of the Mission, including staff complement and footprint;

- the Mission’s budget for administrative services;

- the Mission hardship level;Footnote 3

- nature of the host country’s banking system;

- the Mission’s accounts payable profile;

- the Mission’s expenditure trends; and

- Transparency International’s rating of the host country’s corruption perception index.

As a result of this work, and in consultation with senior officials in the Department, a first phase of Mission audits was initiated in 2016-17 and five Missions that operate in higher fraud risk environments were selected for audit. These were: Abuja (Nigeria); Algiers (Algeria); Moscow (Russia); Nairobi (Kenya); and New Delhi (India). An additional Mission that operates in a lower fraud risk environment, Seoul (South Korea), was selected for comparative purposes.

As part of a second phase of Mission audits initiated in 2017-18, five more Missions that operate in higher fraud risk environments were selected for audit. These were: Amman (Jordan); Cairo (Egypt); Jakarta (Indonesia); Kingston (Jamaica); and Sao Paulo (Brazil). An additional Mission that operates in a lower fraud risk environment, Madrid (Spain), was selected for comparative purposes.

The Embassy of Canada in Indonesia

The Embassy of Canada (the Mission) in Jakarta (Indonesia) is a medium-sized mission comprising 23.5 full time equivalent Canada-based staff (CBS) and 62 locally engaged staff (LES). The Mission is co-located with the Mission of Canada to ASEAN, the Association of Southeast Asian Nations, which was established in 2015-2016 and comprises an additional 5.5 full time equivalent CBS, including a Head of Mission (HOM), and four (4) LES. The Jakarta Mission composition includes the following programs: Common Services and Consular; Development, Foreign Policy and Diplomacy Service; Trade; and Security & Emergency Management. The Mission’s partner departments include Immigration, Refugees and Citizenship Canada; National Defence and the Canadian Armed Forces; Royal Canadian Mounted Police; Export Development Canada; and Agriculture and Agri-Food Canada. The Mission is accredited to Timor-Leste.

Indonesia is the world’s fourth most populous nation, the world’s 10th largest economy in terms of purchasing power parity, and a member of the G-20.Footnote 4Jakarta, the capital, is the largest city in Southeast Asia with an estimated population of more than 10 million people.Footnote 5 Indonesia is a founding member of ASEAN, and one of Canada’s most important partners in the Asia Pacific region. Extreme traffic, poor road infrastructure, unsafe public transportation, and daily protests heavily impact the Mission’s daily operations. Further, the Mission faces challenges relating to the difficult business environment (including competing for qualified local employees), corruption, severe environmental conditions such as flooding, earthquakes, and volcanoes, high pollution levels, language barriers, and terrorism threats. Management also indicated that the limited bandwidth at the two Missions impedes effective communication of data and other information across all programs. Taking these factors into consideration, the Jakarta Mission is designated as a hardship level [REDACTED].Footnote 6

Common Services Program

The Common Services (CS) Program in the Jakarta Mission provides administrative and operational support to both the Jakarta and ASEAN Missions, along with partner departments, and is responsible for all financial transactions and human resources activities. Accountability and responsibility are held by the Head of Mission (HOM). In November 2014, the Mission transitioned to the Common Service Delivery Point (CSDP) in Delhi (India), where it received administrative support until August 2017, when support was transferred to the CSDP in Manilla (Philippines). At the time of the transition, the CS and Consular team was re-organized and resulted in staff reduction and turnover.

The CS Program is managed by a Management and Consular Officer (MCO)Footnote 7 at the FS-03 level. The MCO is supported by a Deputy MCO (DMCO)Footnote 8 at the FS-02 level. The MCO oversees 7 LES in the areas of human resources, finance, IT, and consular services. Table 1 shows the Mission’s Common Services Program expenditures from 2014-15 to 2016-17.

| Fund Centre | Fund | FY 2014-15 | FY 2015-16 | FY 2016-17 |

|---|---|---|---|---|

| Common Services | Operations and Maintenance | 578,363.59 | 817,695.68 | 669,068.39 |

| Capital | 38,159.80 | 80,245.39 | 65,480.51 | |

| LES Salary | 270,060.65 | 277,129.81 | 305,642.96 | |

| Property and Materiel | Operations and Maintenance | 2,120,776.78 | 3,427,985.55 | 3,267,994.75 |

| Total | 3,007,360.82 | 4,603,056.43 | 4,308,186.61 | |

Source: FAS Expenditures Report as of February 7, 2018

The property, materiel, and transportation section is overseen by the DMCO, who is supported by an LE-07 Property & Material Manager. This section is responsible for the oversight and maintenance of the Chancery, Official Residence, Staff quarters (SQs), inventory, and a fleet of vehicles. Table 2 below shows the Mission’s inventory of property and vehicles. In addition, the DMCO is responsible for the transportation section, supervising an LE-05 Protocol and Transportation Coordinator and eight (8) drivers.

| Real Property | Crown-owned | Crown-leased | Total |

|---|---|---|---|

| Official Residence | - | 1 | 1 |

| Chancery | - | 1 | 1 |

| Compound (Recreation Facility that includes 2 bungalows, pool) | 1 | - | 1 |

| Staff Quarters | 27 | 27 | |

| Storage | - | 1 | 1 |

| Parking | - | 4 | 4 |

| Total | 1 | 34 | 35 |

| Vehicle Fleet | Armoured | Standard (soft shell) | Total |

| [REDACTED] | [REDACTED] | [REDACTED] |

Source: Real Property: 2017-18 PRIME database; Vehicles: 2017 Mission Inventory

Consular Program

The Jakarta Mission, through its Consular Program, provides consular services and assistance to Canadians, including passport, citizenship and notarial services. The Consular Program is managed by the FS-03 MCO mentioned above. She is supported by the DMCO and two LES. As part of this service, the Mission is responsible for collecting, safeguarding, recording and depositing consular fees in a timely manner.

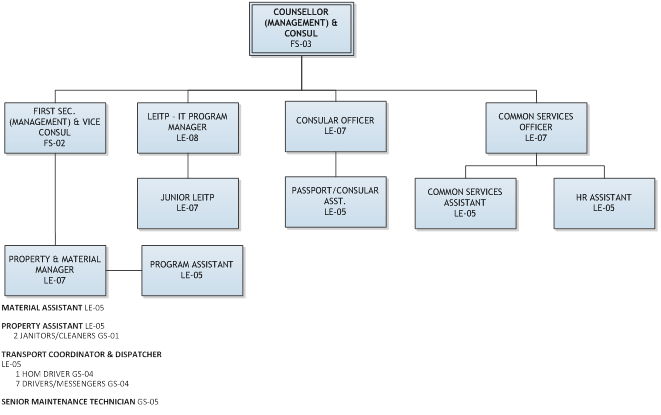

Appendix A shows the organizational chart for the Management and Consular Services Program in the Jakarta Mission.

2. Audit objective and scope

The objective of this audit was to provide assurance that sound management practices and effective controls are in place to ensure good stewardship of resources at the Jakarta Mission to support the achievement of Global Affairs Canada objectives. The audit team examined management practices related to the Management and Consular Services Program at the Mission, specifically in the areas of local procurement, asset management and human resources. Detailed audit criteria are listed in Appendix B.

Audit results were derived from the examination of documentation, data analysis of Mission expenditures and walk-throughs of key common services, property and materiel and consular processes. The audit team conducted work on-site at the Mission from November 20th to December 1st, 2017. A review of a sample of contracts, expenditures, asset disposals, payroll transactions, overtime payments, and staffing actions was undertaken, in addition to an examination of the inventory system. Interviews were conducted with the HOM, CBS management and key LES within the Management and Consular Services Program, as well as staff at Headquarters (HQ). The audit team performed on-site visits to local vendors, the Mission’s bank and a sample of SQs. In addition, the audit team met with two like-minded Missions – Australia and the European Union – to gather information regarding their challenges and good practices in the management of common services.

3. Observations

This section sets out key findings and observations, divided into six general themes: accountability and oversight; planning and budgeting; monitoring; local procurement; asset management; and human resources and LES staffing.

3.1 Accountability and oversight

It was expected that Mission and HQ management would exercise effective oversight of Mission activities and expenditures to ensure proper stewardship of Mission resources. The audit examined roles and responsibilities, as well as key oversight functions, of the Mission management team and key Mission staff from the CS Program.

Accountability for the Jakarta Mission rests with the HOM, who reports directly to the Director General of the Southeast Asia division (OSD). HQ has a role in supporting and enforcing HOM accountability, including the provision of Common and Consular Services. The MCO, who reports to the HOM, is also accountable to the International Platform Branch at HQ. The HOM has been posted to Jakarta since September 2016, while the MCO arrived at the Mission in September 2017.

Key oversight mechanisms are expected to be in place at Missions. The HOM and MCO indicated that they meet weekly to discuss management issues, such as human resources and finances. In addition, they indicated that operations meetings are held every Monday with all managers and HOMs where information regarding operational issues is shared. Further, the audit team found that there was a Committee on Mission Management (CMM) which meets every 2-3 weeks. A review of CMM minutes from FY 2016-17 and 2017-18 found that human resources, procurement and asset management planning, and performance and outcomes were discussed to a limited extent. The committee also did not seem to be well-informed of LES staffing activities. By not using the CMM as a platform to inform management of staffing activities and other key operational priorities, the Committee is not being effectively utilized to provide oversight and strategic direction. In addition, until October 2017, the CMM did not have a Terms of Reference (ToR) to guide the activities of the Committee. However, with the recently approved ToR, members will have a clear guidance in regard to the mandate of the committee and their specific roles and responsibilities.

There is a Regional Contract Review Board (RCRB) in place at the CSDP in Manilla (Philippines). Jakarta is a new member, having recently transitioned from CSDP Delhi (India). The RCRB is intended to provide oversight and a challenge function to missions prior to entering in large contracts in order to protect the Department’s interests. Based on a review of contracting activities, the audit team found the Jakarta Mission did not engage the RCRB prior to signing a contract, as required. As result, the Mission did not follow procurement procedures, and did not benefit from the RCRB’s oversight and insight on contracting practices.

The LES play key roles in supporting Mission management through their subject-matter, cultural and linguistic knowledge. While many key LES Common Services staff are relatively new to the Mission, they indicated to the audit team that they understand their roles and responsibilities related to human resources, procurement, and asset-management.

3.2 Planning and budgeting

It was expected that planning and budgeting would be based on need and there would be a rationale for planned activities and forecasted expenditures. The Mission uses Strategia, the corporate integrated planning and reporting tools, for its annual financial planning exercise. This ensures that the Mission’s financial planning and budgeting aligns with departmental planning commitments.

When planning for the upcoming fiscal year, the Mission reviews its historical expenditures and makes adjustments for events which are anticipated to affect budget requirements. However, the Mission does not have planning processes in place for procurement, property and material management, and fleet management.

Over the past three years, the Mission’s planned expenditures have varied significantly from actual expenditures. Variances between budgets and actual expenditures showed that in FY 2015-16, spending increased nearly 60% in all common service and property areas. Although Mission operations have grown due to the opening of a new mission (ASEAN) co-located inside the Jakarta Chancery, this does not account for all of the variances. The Mission forecasted less than the spending for rent required for the Chancery and SQs, in both FY 2015-16 and FY 2016-17, despite the reoccurring nature of these expenses. In addition, the audit team found that expenditures on goods and supplies were often not linked to a planning process, need assessment, or life cycle. For example, the audit team noted a practice to replace all small appliances (kettle, coffee maker, etc.) in SQs at time of rotation, regardless if the items have passed their useful life. Furthermore, the audit team found that expenditures at year-end represented 35% of overall spending in these areas. Staff indicated these purchases were made because money was available.

Without a strong planning and budgeting processes based on need and asset life cycle, Management’s ability to properly forecast expenses is limited. Unexpected year-end budget surpluses can result in excessive purchases of goods, leading to increased risk of asset losses, obsolescence of assets, and higher storage costs.

3.3 Monitoring

It was expected that monitoring activities would be performed to provide general information on Mission compliance with Government of Canada and department specific policies and procedures.

The expected monitoring over procurement-related activities is limited to periodic review of expenditures against budgets. No monitoring is done to ensure proper procurement methods are being used, or if the level of vendor utilization is appropriate. The audit team found the Mission has a lack of formal procurement mechanisms in place, and that business is concentrated to a few vendors without competitive processes. Without strong monitoring of procurement activities, the Mission will not be able to assess if this function is properly supporting Mission operations and providing value for money.

The Mission has some monitoring activities in place for financial operations, including review of FINSTAT reports and burn rate reports by mission management. However, some gaps were noted with the Mission’s monitoring in regard to bank reconciliations and coding errors. For example, the Mission was not taking steps to correct discrepancies identified by the CSDP in the bank reconciliation in a timely manner. A review of monthly bank reconciliations revealed delays in making adjustments for more than two months, and some dated back to 2015. Without proper due diligence and monitoring of the Mission’s bank account and bank reconciliations, the Mission is less likely to detect variances, errors, and potential fraudulent activities.

In addition, the audit team noted transaction coding errors for significant expenditures, such as rent, service charges, and security deposits. This reduces the accuracy of budgeting and forecasting, as well as recording properly prepaid expenses in FAS and tracking of refundable advances.

Further, the audit team found evidence of a lack of monitoring and challenge function by Mission management and HQ over the Mission’s requests for vendor creation and amendment. As the Mission does not have access to create or modify vendor accounts, approved requests must be sent to Financial Operations, International (SMFF) at HQ for processing. The audit team found instances of vendor creation and amendment where the vendor’s name, email, and banking details, were for an individual rather than the business name appearing on invoices. [REDACTED] Without proper monitoring of vendor accounts, the Mission may make inappropriate payments to improper individuals or entities, and expose itself to legal, financial and reputational risks.

Overall, there are insufficient monitoring activities being performed at the Mission and HQ, resulting in issues of financial operations, purchasing, expenditures and budget planning and reporting, which prevent accurate forecasting, the identification of problems, and the possibility of corrective action, thereby increasing the risk of financial loss.

3.4 Local procurement

The audit team expected that procurement of goods and services would be in compliance with Treasury Board Contracting Policy and would achieve the best value for money. The audit team examined the mechanisms and tools in place to procure goods and services at the Mission. To that effect, a sample of 38 procurement transactions and contracts, covering the period between August 2015 and September 2017, was reviewed.

Procurement and Contract Management

The audit team reviewed 38 procurement transactions, eight (8) of which had contracts and/or purchase orders in place. The audit team expected that these sampled contracts would be established and managed as per procurement policies and procedures to ensure fairness, transparency, and value for money. The audit team, however, found the following issues:

- Two (2) instances where purchase orders were put in place after the goods/services were provided and invoice was received, rather than at the initiation of the procurement, as required.

- A sole source contract over $10,000 signed without prior review by the Regional Contract Review Board. The contract was also not registered in FAS Material Management module upon initiation, as required.

- Two (2) instances where the justifications for sole source contracts did not include sufficient detail to support a non-competitive method of procurement.

The audit team expected to find that formal contracting mechanisms would be implemented by the Mission for reoccurring services such as cleaning, moving, and regular property maintenance. Of the 38 procurement transactions reviewed by the audit team, 15 were for these types of service. In reviewing these 15 transactions, the audit team found only three (3) instances where a purchase order or contract was used. The Mission has not been actively using service contracts or Standing Offer Agreements (SOA) to procure regular services.

Acquisition cards are a procurement method used to help reduce the administrative burden in the process, and the audit team expected to find effective control in place to ensure these transactions are in line with policies and procedures. Based on a review of acquisition cards purchases, the audit team found control gaps with the way the cards were being used. For example, an acquisition card was used as the method of payment for a large volume of reoccurring monthly transactions for fumigation services, as opposed to establishing a formal service contract with monthly invoicing. Acquisition cards were also used for a wide variety of regularly purchased goods (equipment and supplies) through a distributor without any formal competitive procurement process.

In addition, the audit team identified a number of control weaknesses and breakdown based on the review of the sample of transactions. These include:

- Lack of competition when initiating services (multiple formal quotes not sought);

- Lack of estimates provided by vendors in advance of work done in order to control costs and ensure value for money;

- Weak pre-approval and/or pre-authorization at initiation stage of service or good procurement. No formal evidence on file to support approved initiation.

- Lack of evidence of price comparison from multiple vendors for acquisition card purchases.

Without fair and competitive service contracts, or SOAs, or supply arrangements in place it is difficult for management to formalize services and goods expectations, control costs, establish service frequency, and to ensure Mission is getting the best value and quality for money.

The Mission has not leveraged competition contracting mechanisms to avoid any preferential or unfavourable treatment of vendors. The audit noted that the Mission selects vendors and procures services on an ad-hoc and ongoing basis using the same vendors selected by Mission property staff. For example, two vendors received two-thirds of property repairs and maintenance related payments during the last two fiscal years without contracts or evidence of competitive selection processes.

Overall, the audit team found significant gaps in the management of procurement processes, including issues with the selected method of procuring, the initiation and management of contracting processes, and the achievement of value for money. These weaknesses in controlling procuring activities leave the Mission exposed to the risk of not receiving quality services at competitive prices from reliable vendors, and therefore unable to meet their operational needs.

Receipt and Payment

The audit team expected that the Mission had effective controls in place to ensure procurement expenditures are accurate, appropriate, and legitimate.

The audit team found a lack of due diligence by management in exercising certification that goods or services have been received and payment can be issued under section 34 of the Financial Administration Act (FAA). Although this approval was signed for all transactions, the receipt of procured goods or services could not be confirmed in all cases. The review of the selected transaction revealed a lack of information confirming receipt of goods or services in line with the quantity and quality ordered. For example, individuals exercising FAA Section 34 on invoices were provided with very limited details about the work performed and pricing. As well, the audit team noted instances where signed job reports were available to support the approval of the invoice, however, there is no evidence they were provided to support the approval of FAA Section 34. Further, in one sample reviewed, it was noted that the Mission approved payment on an invoice where the quantity billed was more than the quantity received (based on the vendor’s delivery notices provided). This represented a loss of $640 CAD. An examination of acquisition card transactions found that formal pre-authorizing purchases, and support to confirm that goods were received or services rendered (FAA Section 34) was lacking.

In addition, the audit team found three (3) instances where duplicate payments were made to vendors, representing a total value of $1,942 CAD. The multiple payments for the same invoices occurred when they were uploaded twice to SAP for payment processing by the CSDP. Neither mission management, nor the CSDP, caught the mistake and excess payments were issued. The audit team alerted the mission to the issue, and efforts to recover the amounts are underway.

The review of payment transactions conducted on-site revealed weaknesses in controls over the process of issuing and cashing mission cheques. The audit team noted that cheques issued to vendors or internal clients (CBS or LES) were being endorsed and cashed [REDACTED] in order to make cash payments. Endorsed cheques should not be used as a mechanism to facilitate a cash payment to a vendor as it is not an appropriate method of payment, and may lead to loss or misappropriation of untracked cash.

The lack of due diligence in approving invoices and acquisition card purchases (section 34), combined with a lack of properly tracking received goods and service rendered and weakness in the management of inventories (as described later in this report) can result in loss of funds through overbilling, non-receipt of goods, or inferior goods being provided. The absence of pre-approving acquisition card purchases can lead to improper purchases. Weak monitoring of processing approved invoices has led to multiple duplicate payments, and leaves the Mission at risk of additional financial losses.

3.5 Asset management

Another area of risk identified by the audit team concerned the management of assets at the Mission, specifically the management of inventory, properties, vehicles, petty cash and consular revenues.

Inventory Control and Disposal

It was expected that once an asset was purchased, it would be recorded, safeguarded, tracked through its life cycle and disposed of in accordance with the Department’s Materiel Management Manual. The Mission has an inventory of properties that includes Crown-leased, and a Crown-owned building tracked in the Physical Resources Information – Mission Environment (PRIME). There are also four types of materiel inventory repositories: information technology equipment; fine art; Chancery, SQ and OR-related assets; and storage located near the Chancery building. The audit team found that the fine art inventories were adequately tracked and safeguarded. The Mission also has an inventory of 11 vehicles, tracked in the Finance and Administration System (FAS) from purchase to disposal.

The audit team noted that at the time of the audit, most SQ inventory lists were created when CBS tenants moved in and were not being updated as items were moved or added. A large volume of furniture, equipment and supplies (household furniture, large and small appliances, electronic items) is held in a storage facility next door to the Chancery office tower; however there was no inventory list of items held in this facility. It was also noted that the Mission was not using the corporate inventory tracking system, Radio Frequency Identification (RFID), was not tracking items using a unique identifier (e.g. inventory number, bar code), and was not capturing sufficient life cycle details (for example, year of purchase, make, model and condition) on inventory lists to accurately and effectively track assets. The general lack of rigour with regards to inventory management increases the risk of misappropriation of assets, and poor asset life cycle management. It was noted that the Mission had recently begun using a spreadsheet to inventory and track goods in the Chancery, the OR, and a selection of SQs. Once completed this spreadsheet is intended to act as an evergreen inventory list, and will capture key details such as purchase date, description, and location.

The audit team noted that warehouse has almost reached his storage capacity, and much of the space is taken up with old goods destined for disposal. Discussions with staff indicate that a shipping container of new furniture from Canada has arrived, and is being stored by the shipping company, at additional cost to the Mission, due to the lack of storage space. Mission management was made aware of this issue, and has expressed an intention to prioritize the auction of the old goods during next rotation season in order to maximize current storage capacity, and to eliminate unnecessary storage expenses.

The audit team examined the disposal of a selection of surplus goods through auctions. The review of the sale noted that the Mission used a third-party auction company which is a good practice. However, since the Mission had not been effectively tracking inventory, including life-cycle details and purchase date, it is difficult to determine whether the assets were in a condition that warranted disposal.

Property Management

Based on a review of property management processes and practices, the audit team noted that the Mission does not do significant formal advanced planning for property repairs and maintenance activities, and contracts are not in place for reoccurring maintenance activities. The audit team found that the Mission is undertaking a large volume of maintenance activities on the Chancery, OR, and SQs, despite the entire property portfolio being leased. A key driver of this trend is that leases in place for SQs include a clause stipulating that small repairs and maintenance jobs, defined as up to either $100 or $200 USD (depending on the lease), would be the responsibility of the Mission, rather than the landlord. This is illustrated by the Mission spending over $120 K in FY 2016-2017 to maintain the leased OR and SQs through a large volume of low-dollar-value transactions (over 600 transactions with approximate median spend of $87 CAD and average of $200 CAD). As a result, the Mission indicated its intention to change current leasing practices by phasing out the small repair lease clause, leaving the landlord fully responsible.

Aside from air conditioner maintenance and some expenses related to relocation season, the majority of transactions appear to be small projects on the OR and unplanned SQ maintenance, such as emergency repairs and CBS requests (usually generated by Mission Request Online (MRO) submissions). These expected or requested maintenance jobs can be attributed to approximately half the transactions from 2016-17, leaving around 300 transactions where the reason for initiation of the work, or the need, is unclear. Without the ability to link transactions to a planning process, or a formal initiation of unplanned expenditures (such as an MRO), the Mission has exposed itself to the risk of unnecessary, redundant, or falsified maintenance transactions being invoiced to the Mission.

[REDACTED]

Fleet Management

It was expected that the Mission would manage its fleet in accordance with the Department’s Mission Fleet Management Guidelines and have a Mission transportation policy outlining proper conduct and management of the Mission fleet. The Mission has such a policy, approved by CMM in September 2017, which details appropriate use of Mission vehicles.

The audit team found that a maintenance tracking sheet is maintained by the Mission’s fleet coordinator to track regular maintenance and periodic breakdown/accident repairs. In addition, the fleet coordinator maintains a driver shift and car rotation schedule, which supports the scheduling of daily requested trips by mission staff. The audit team also noted that a daily log is kept for each vehicle which details each trip taken.

Fuel for vehicles is purchased through one established vendor using fuel cards designated to each vehicle. The Mission receives a monthly fuel purchase statement that details the quantity, charge, vehicle, and often the odometer reading. Gas purchases and receipts are also tracked in a log, and signed off by the driver. The Fleet coordinator indicated that these records are periodically reviewed to identify issues with the frequency of fuel purchases, but detailed fuel consumption analysis is not done. The audit team conducted a fuel consumption reasonability tests using mission data, and noted a number of vehicles whose fuel consumption was unreasonably high compared to KMs travelled.

Fleet vehicles also each have a Toll debit card used to electronically pay road tolls. While purchases using fuel cards are actively monitored, the use of toll cards are not, and are simply refilled when the balance is low. Without monitoring there is a risk that these cards could be used for inappropriate purchases, as they can also be for any type of goods.

Based on concerns raised by the HOM regarding fleet size, the audit team conducted a comparison analysis on the usage of four (4) Mission fleet vehicles and found that all four (4) were underutilized against Treasury Board and GAC guidelines (80% working days used or 20,000 Km per year). The Mission Fleet Management Guidelines recommend that a fleet utilization review be done by missions to ensure fleet size is appropriate. The HOM has indicated that actions are already underway to reduce the number of vehicles to an optimal level.

The audit team examined the Mission’s disposal of four (4) fleet vehicles. The review found no significant issues with the documentation, however, the audit team did find that the Mission was not effectively tracking and safely securing diplomatic license plates that are no longer in use. The potential loss or theft of a Canadian diplomatic license plate represents a security and reputational risk.

Petty Cash

The Mission requires a cash supply for small, urgent or unique purchases not covered by other means. The Mission has [REDACTED] petty cash account [REDACTED] at the time of audit. The Mission mostly manages its cash in accordance with relevant policies and legislative requirements. However, some concerns were noted. For example, it was noted that some requirements from the Department’s Procedures on Petty Cash for Missions are not being observed, including a lack of surprise petty cash counts, transaction splitting to avoid limits, transactions exceeding petty cash limits, and transactions without original receipts. The petty cash account was reconciled during the surprise counts performed by the audit team and the funds are securely stored with appropriate access.

Consular Revenues

It was expected that fees collected for consular services would be properly accounted for, reconciled, safeguarded and deposited as required. An examination of consular revenues management revealed that the Mission receives cash and keeps copies of the official receipts with the related consular service applications. However, the Mission does not use sequential receipts when providing receipts to clients and when conducting reconciliation activities. Further, reconciliations between revenues and receipts are performed much less frequently than required by departmental procedures (every 1-3 months instead of daily). As a consequence, the Mission does not make regular deposits of consular revenues in its bank account. This was supported by a review of consular revenues included in the Mission’s bank reconciliations for a 12-month period from April 2016 to March 2017. There was an instance where cash was kept on hand for over 450 days. There is also a lack of proper segregation of duties and controls over the cash handling process.

Without strong controls over handling consular cash, there is an elevated risk of undetected losses. To mitigate the risk related to handling cash, the Mission decided to no longer accept local currency cash payment for consular services. As of January 2018, the Mission is only accepting payment by credit cards and cash in Canadian dollars to pay consular services, which represents approximately 5% of cash payments.

3.6 Human Resources and LES staffing

The audit team examined staffing files to determine whether adequate human resources management practices and controls were in place. It was expected that staffing actions would be in compliance with relevant policies and procedures, conducted in a fair, open and transparent manner, and that staffing files would contain the required documentation.

The audit team examined a sample of five (5) LES staffing actions, and found that two (2) staffing action files were incomplete, as key documentation was not retained or complete. Also, in one case, the successful candidate did not meet an essential qualification to be fluent in spoken English, and should not have been qualified and selected in that process. Due to the breakdown of these controls over staffing, the Mission may have difficulty demonstrating that staffing actions were conducted in a fair, open, and transparent manner.

A sample of the personnel files of five (5) LES was also reviewed to ensure the retention of required documentation, such as job descriptions, performance agreements and any documentation related to values and ethics and disciplinary actions. The audit team found that the personnel files reviewed were properly documented.

It was expected that there would be a process to manage overtime that is aligned with departmental policies, including pre-approval, rationale and approval, monitoring, and reporting. The review of a sample of Common Service LES overtime showed that the overtime hours worked were warranted and appeared reasonable, however, none had been pre-approved. At the time of the audit staff indicated that pre-approval is not a practice for drivers, nor is it practiced for the Property team during rotation season. However, as per minutes of a CMM meeting in November 2016, management decided to require pre-approval for overtime in all cases. By not enforcing the requirement for overtime pre-approval, there is a risk that excessive or unnecessary overtime can be claimed and overtime budgets can be exceeded.

4. Conclusion

The audit concluded that there were significant weaknesses in the management practices and controls in place to ensure sound stewardship of resources at the Jakarta Mission. There is a lack of management oversight and monitoring in the areas of local procurement, asset management, consular revenue and inventory management. The Mission does not leverage available information to support decision-making and to promote good stewardship of resources. Some processes established by Headquarters relating to finance, procurement, contracting and human resources are not consistently followed and some key controls are not in place or not being followed.

[REDACTED]

The audit team verbally debriefed the HOM and the MCO after completion of work on-site. As a result, Mission management has immediately taken many measures to address issues identified by the audit.

5. Recommendations

Recommendations to the Jakarta Mission:

- The Head of Mission should ensure that responsibilities and accountabilities of Canada-based staff and Locally-Engaged Staff in the Property and Materiel Section with regards to procurement, contracting and asset management are clear and communicated.

- The Head of Mission should take measures to strengthen planning, oversight, controls and monitoring with respect to property (including the enforcement of lease agreements and the process surrounding repairs and maintenance) and fleet management.

- The Head of Mission should take measures to strengthen oversight, controls and monitoring to ensure that procurement and contracting processes comply with governmental policies and regulations and provide value for money, with corrective actions when non-compliance is detected.

- The Head of Mission should ensure that proper management of the inventory cycle is undertaken, including recording, tracking and maintaining inventory

- The Head of Mission should take appropriate measures to enhance compliance of the Mission’s financial operations with the Department’s directives and procedures, especially, in the area of transaction coding, use of Mission cheques, vender accounts, and accounting for Mission bank transactions in FAS.

Recommendations to Headquarters:

- The Assistant Deputy Minister of the International Platform Branch (ACM) should reassess the use of RFID as the formal corporate inventory system for missions. In the meantime, and in order to mitigate the current risks, the Assistant Deputy Minister of the International Platform Branch should communicate to the missions clear expectations and provide guidance for adequate life cycle management of their inventory to ensure proper due diligence.

- The Assistant Deputy Minister and Chief Financial Officer, Corporate Planning, Finance and Information Technology Branch, should enhance monitoring and challenge over the creation and amendment of vendor accounts in the Financial and Administration System.

- The Assistant Deputy Minister of the International Platform Branch (ACM) should take timely and appropriate measures to ensure that legal and financial liabilities associated with the crown-owned [REDACTED] are minimized.

Appendix A: Organizational chart for the management and consular services program

The organizational chart shows the structure of the Management and Consular Services Program at the Mission in Jakarta and the reporting relationships. At the top of the hierarchy, there is the Counsellor (Management) & Consul (FS-03). The following positions report to the Counsellor (Management) & Consul:

Text version

Appendix B: About the audit

Objective

The objective of this audit was to provide assurance that sound management practices and effective controls are in place to ensure good stewardship of resources at the Jakarta Mission to support the achievement of Global Affairs Canada objectives.

Scope

The scope of the audit included those management practices and controls in place to support the Jakarta Mission operations. Specifically, the audit examined processes related to the management of consular revenues, procurement and asset management (including property, vehicles, cash and materials). Human resource processes relating to LES staffing actions, LES payroll and overtime were also examined.

The most up-to-date documentation available as at September 2017 was reviewed. In addition, Common Services Program expenditures and data for property and fleet were examined from 2014-15 to 2016-17. A sample of files and transactions were tested from activities that took place from 2015-16 to 2017-18, as shown in Table 3.

| Description of Testing Sample | Number of samples |

|---|---|

| Procurement transactions with associated contract or purchase order | 8 |

| Procurement transactions through direct purchase (no associated contract or purchase order) | 19 |

| Petty cash transactions | 3 |

| Acquisition Card transactions | 8 |

| Overtime transactions | 4 |

| Visits to staff quarters to review maintenance work and on-site inventory | 3 |

| Disposed asset files | 5 |

| LES staffing action files | 5 |

| LES personnel files | 5 |

| Total | 60 |

Criteria:

Criteria were developed based on a detailed risk assessment.

Criterion 1: Adequate and effective oversight and accountabilities are in place to support stewardship of Mission resources.

- 1.1 Management exercises effective oversight of procurement, asset management and human resource activities.

- 1.2 Authorities and accountabilities for procurement, asset management and human resources are clear, communicated and understood.

- 1.3 Planning processes are in place for procurement, asset management and human resources, which consider needs, asset life cycle, and resources.

- 1.4 Monitoring and reporting of procurement, asset management and human resource activities take place to inform decision-making.

Criterion 2: Effective management practices and controls are in place to ensure stewardship of Mission resources and compliance with relevant policies and legislative requirements.

- 2.1 Effective controls are in place to ensure that procurement of goods and services comply with relevant policies and legislative requirements and achieve value for money.

- 2.2 Effective controls are in place to ensure that procurement expenditures are accurate, appropriate, and legitimate.

- 2.3 Inventory control and asset management practices are adequate and appropriate.

- 2.4 Cash is managed in accordance with relevant policies and legislative requirements.

- 2.5 LES staffing actions comply with relevant policies and legislative requirements and are fair, open and transparent.

- 2.6 LES salaries and overtime payments are accurate and complete.

Approach and Methodology:

In order to conclude on the above criteria, and based on identified and assessed key risks and internal controls associated with the related business processes, the audit methodology included, but was not limited to the following:

- Documentation review (budgets, business plans in Strategia, property management plans etc.)

- Walkthrough of key common services, property and materiel, and consular processes

- Data analytics of Management and Consular Services Program expenditures

- File testing (contracts and expenditures relating to Common Services Program, payroll, overtime costs and staffing actions)

- Interviews (Head of Mission, CBS management and key LES of Management and Consular Services Program and relevant employees at HQ and Common Service Delivery Point)

- Inventory testing

- Petty cash counts

- On-site examination of Chancery, storage facilities and a sample of staff quarters

- Comparisons with like-minded Missions

- Visits to a sample of local vendors

- Visit to Mission bank

Appendix C: Management action plan

| Audit Recommendations to Jakarta Mission | Management Action Plan | Area Responsible | Expected Completion Date |

|---|---|---|---|

|

| Head of Mission - Jakarta | March 31, 2018 |

|

| Head of Mission - Jakarta | July 2018 for all items |

|

| Head of Mission - Jakarta | March 31, 2018 |

|

| Head of Mission - Jakarta | June 30, 2018 |

|

| Head of Mission - Jakarta | January 31, 2018 |

| Audit Recommendation to Headquarters | Management Action Plan | Area Responsible | Expected Completion Date |

|---|---|---|---|

|

| The Assistant Deputy Minister of International Platform Branch- ACM |

|

|

| The Assistant Deputy Minister and Chief Financial Officer (CFO), Corporate Planning, Finance and Information Technology Branch - SCM |

|

| Physical Resources Bureau (ARD) is re-evaluating disposal options for this property and working with local real estate agents to determine the most cost effective option. There are legal questions concerning the property’s boundaries. Mission is consulting local lawyers on this and awaiting further advice on guidance on options to resolve the issues. | The Assistant Deputy Minister of International Platform Branch -ACM | March 2019 |

Appendix D: Acronyms

- ACM

- International Platform Branch

- ADM

- Assistant Deputy Minister

- ASEAN

- Association of Southeast Asian Nations

- CS

- Common Services

- CBS

- Canada-based staff

- CFO

- Chief Financial Officer

- CSDP

- Common Service Delivery Point

- CMM

- Committee on Mission Management

- DMCO

- Deputy Management and Consular Officer

- FAA

- Financial Administration Act

- FAS

- Finance and Administration System

- FINSTAT

- Financial Status report

- HOM

- Head of Mission

- HQ

- Headquarters

- IT

- Information Technology

- LES

- Locally Engaged Staff

- MCO

- Management and Consular Officer

- MRO

- Mission Request Online

- OGM

- Asia Pacific Branch

- PRIME

- Physical Resources Information - Mission Environment

- RCRB

- Regional Contract Review Board

- RFID

- Radio Frequency Identification Device

- SCM

- Corporate Planning, Finance and Information Technology

- SMFF

- Financial Operations, International

- SOA

- Standing Offer Agreement

- ToR

- Terms of Reference

- SQ

- Staff Quarter

- Date modified: