Quarterly economic and trade report – Q4 2022

Highlights

- Global economic growth slowed to 1.2% in the fourth quarter (Q4) of 2022, from 3.9% growth in Q3. High inflation, tight financial conditions, COVID-19 outbreaks in China, and the War in Ukraine all contributed to the slower activity.

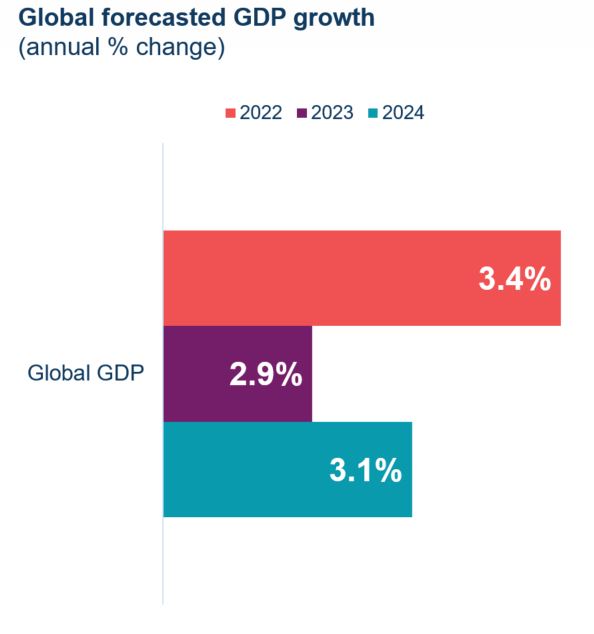

- The International Monetary Fund forecasts global growth to slow to 2.9% in 2023, led by advanced economies, which are expected to grow only by 1.2%. Emerging market growth is forecasted to increase slightly to 4.0% in 2023.

- The Canadian economy finished 2022 on a flat note, posting 0.0% (annualized) growth in Q4 of 2022. A boost from net trade offset significant contractions in inventories and a continued contraction in investment and housing. Meanwhile, fourth-quarter consumption rebounded from soft growth in Q3.

- While the volume of goods and services trade contributed to growth, the value of Canada’s goods and services exports (-1.0%) and imports (-1.2%) decreased in Q4 of 2022. A contraction in goods exports outweighed robust growth in services exports.

- As the effect of increased interest rates continues to impact consumption and the housing sector, the Bank of Canada expects Canadian economic growth to slow to 1.0% in 2023 from 3.4% in 2022. However, high-frequency indicators from February 2023 suggest that the year started stronger than expected. Economic activity is expected to pick up modestly in 2024, with growth forecasted to come in at 1.8%.

Table 1: Highlights – fourth quarter 2022

| % change, Q3 2022 vs Q2 2022 | % change, 2022 v 2021 | |

|---|---|---|

| Global real GDP* | 1.2 | 3.1 |

| Global merchandise trade volume | -2.1 | 3.2 |

| Canadian real GDP* | 0.0 | 3.4 |

| Canadian exports (goods & services) | -1.0 | 21.0 |

| Canadian imports (goods & services) | -1.2 | 20.3 |

Notes: *Throughout the report, GDP is quarterly changes at annualized rates.

Source: Oxford Economics, Netherland Bureau for Economic Analysis, Statistics Canada.

Global economic growth slowed in Q4

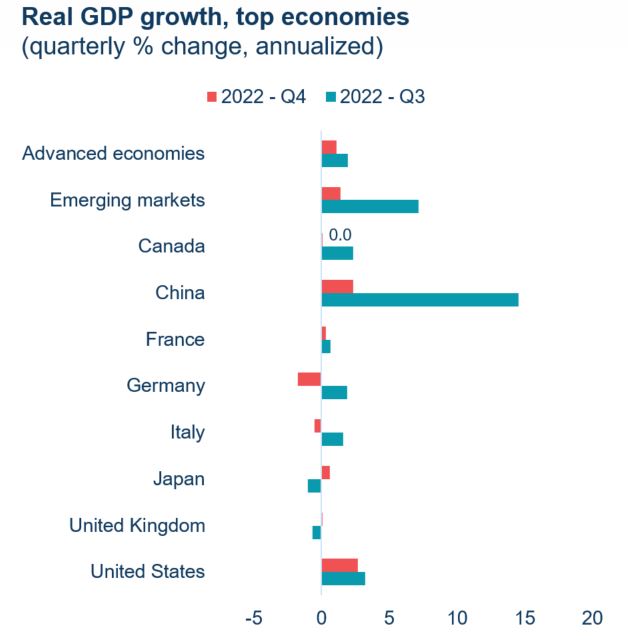

Global economic growth slowed as 2022 came to a close, increasing 1.2% in the fourth quarter (Q4) after posting strong growth in Q3 (3.9%). The slowdown was sharper in emerging markets, which posted 1.4% growth in Q4 of 2022 compared to 7.1% in Q3. Growth in advanced economies slowed to 1.1% in Q4 from 1.9% in Q3.

The U.S. economy was more resilient than expected, advancing 2.7% in Q4 of 2022, following 3.2% growth in Q3. Consumption supported growth in Q4 as Americans dipped into their savings – the personal savings rate in the U.S. reached record lows at the end of 2022 – while the job market held tight. This strength ultimately led the Federal Reserve to tighten rates again at the start of 2023. Meanwhile, growth slowed across many European economies, with the Eurozone economy contracting by 0.1% in Q4 of 2022 after increasing by 1.5% in Q3.

In emerging markets, China’s economy slowed significantly in Q4, increasing by only 2.3% compared to 14.5% in Q3. Several COVID-19 outbreaks across the country and continued challenges in its property market, weighed on Chinese economic growth. The year 2022 marked the slowest expansion for China in the past two decades.

On a cautiously optimistic note, inflation started to show signs of potential slowing at the end of 2022. According to IMF estimates, global inflation for the median economy slowed to 7.1% in December 2022. While still high, this is down from a peak of roughly 8.3% in August 2022. However, core inflation was stickier and remains high, suggesting that the problem is not yet solved.

Sources: Oxford Economics, Statistics Canada. Seasonally adjusted. Retrieved on 2023-03-10.

Text version

| Real GDP growth, top economies (quarterly % change, annualized) | 2022 - Q3 | 2022 - Q4 |

|---|---|---|

| Advanced economies | 1.9 | 1.1 |

| Emerging markets | 7.1 | 1.4 |

| Canada | 2.3 | 0.0 |

| China | 14.5 | 2.3 |

| France | 0.7 | 0.3 |

| Germany | 1.9 | -1.7 |

| Italy | 1.6 | -0.5 |

| Japan | -1.0 | 0.6 |

| United Kingdom | -0.7 | 0.1 |

| United States | 3.2 | 2.7 |

Q4 world trade and production volumes contract

World merchandise trade volumes contracted by 2.1% in Q4 of 2022, following modest growth in Q3 (1.3%). Export volumes in advanced economies decreased by 1.0% in Q4, led by a contraction in U.S. exports (-2.6%). Eurozone exports (-0.2%) also pulled volumes down, while exports from the United Kingdom (+0.9%) and Japan (+0.8%) bucked the trend.

Export volumes in emerging economies (-4.0%) contracted for the second consecutive quarter. The contraction was widespread across markets. Activity in China continued to be challenged by the nation’s zero-COVID policy, with export volumes declining by 5.5% in Q4. The December lifting of the zero-COVID is expected to support trade growth in 2023.

After increasing by 1.2% in Q3 of 2022, world industrial production volumes decreased by 0.8% in Q4. The contraction was greater in advanced economies (-1.1%) compared to emerging markets (-0.5%). Modest growth in China (0.5%) partially offset contractions elsewhere in emerging Asia, Latin America, and Africa and the Middle East.

Source: Netherland Bureau for Economic Analysis, retrieved on 2023-03-10.

Text version

| World merchandise trade and industrial production volume (Index 2010 = 100) | World merchandise trade volume | World industrial production volume |

|---|---|---|

| Jan-20 | 120.7 | 120.1 |

| Feb-20 | 120.8 | 120.8 |

| Mar-20 | 118.2 | 120.3 |

| Apr-20 | 104.4 | 109.8 |

| May-20 | 104.4 | 110.9 |

| Jun-20 | 111.9 | 116.1 |

| Jul-20 | 117.3 | 119.9 |

| Aug-20 | 119.7 | 121.4 |

| Sep-20 | 123.0 | 123.2 |

| Oct-20 | 123.8 | 124.4 |

| Nov-20 | 125.8 | 125.6 |

| Dec-20 | 126.6 | 127.0 |

| Jan-21 | 127.1 | 128.5 |

| Feb-21 | 126.9 | 128.2 |

| Mar-21 | 131.0 | 128.7 |

| Avr-21 | 130.4 | 129.3 |

| May-23 | 129.0 | 128.2 |

| Jun-21 | 129.5 | 129.5 |

| Jul-21 | 128.8 | 129.7 |

| Aug-21 | 129.8 | 129.3 |

| Sep-21 | 129.4 | 128.3 |

| Oct-21 | 130.9 | 129.4 |

| Nov-21 | 134.4 | 131.0 |

| Dec-21 | 135.9 | 132.4 |

| Jan-22 | 133.8 | 133.8 |

| Feb-22 | 134.7 | 135.1 |

| Mar-22 | 133.0 | 133.6 |

| Apr-22 | 132.8 | 131.0 |

| May-22 | 135.8 | 132.0 |

| Jun-22 | 134.9 | 133.8 |

| Jul-22 | 135.0 | 133.3 |

| Aug-22 | 136.7 | 134.0 |

| Sep-22 | 137.0 | 134.2 |

| Oct-22 | 135.4 | 133.0 |

| Nov-22 | 133.0 | 132.8 |

| Dec-22 | 131.8 | 132.6 |

Economic growth to slow in advanced economies and pick up modestly in emerging markets

The International Monetary Fund (IMF) forecasts global growth to slow to 2.9% in 2023 as high inflation, a rise in central bank rates, and the War in Ukraine continue to constrain growth.1 A sharp and widespread decline in growth is expected amongst advanced economies, with growth slowing from 2.7% in 2022 to 1.2% in 2023. Meanwhile, growth in emerging markets is forecasted to pick up slightly, increasing to 4.0% in 2023 from 3.9% in 2022.

Amongst advanced economies, U.S. economic growth is expected to decrease from 2.0% in 2022 to 1.4% in 2023 on increasingly tight financial conditions. Russia’s War on Ukraine will continue to impact growth in Europe, with Euro Area growth slowing from 3.5% in 2022 to 0.7% in 2023. The United Kingdom’s economy is expected to shrink in 2023, contracting 0.6%.

In emerging markets, the lifting of China’s zero COVID policy in December boosted its 2023 outlook. China’s economic growth is expected to be 5.2% in 2023, up 0.8 percentage points from the IMF’s October 2022 outlook. Growth in India, Indonesia, and other emerging Asia countries is expected to slow. Likewise, growth in Latin American and the Caribbean is expected to decline, constrained by tight financial conditions and lower export prices. The Middle East and Central Asia will also experience slowing growth, driven, in part, by lower oil production.

While their global outlook for 2023 is slow compared to growth over the past two decades, the IMF is far from having the slowest forecast. For example, the World Bank forecasts the global economy will expand by 2.2% in 2023, while Oxford Economics, a private sector forecaster, expects 2023 growth to be roughly 2.1%. The ultimate impact of widespread monetary policy tightening, whether and when inflation will slow, and the War in Ukraine remain primary sources of uncertainty.

1. IMF, World Economic Outlook, January 2023.

Source: IMF World Economic Outlook, January 2023, retrieved on 2023-01-30.

Text version

| 2022 | 2023 | 2024 | |

|---|---|---|---|

| Global forecasted GDP growth (annual % change) | 3.4 | 2.9 | 2.1 |

The Canadian economy stalled in the fourth quarter

After five consecutive quarters of relatively strong performance, Canadian economic growth was essentially unchanged (0.0% annualized) in the fourth quarter of 2022. Net trade added 4.7 percentage points to growth in Q4, as a contraction in imports (12.0%) and weak growth in exports (0.8%) both boosted growth. A substantial decrease inventories accumulation, particularly in manufacturing and retail and wholesale durables, offset the positive contribution from trade, subtracting 5.6 percentage points from growth in Q4 of 2022.

While the economy stalled, the underlying story is nuanced, as a tight job market supports spending while interest rates are dragging down investment and housing. Consumption contributed 1.6 percentage points to GDP growth in Q4 of 2022, as it rebounded from a soft third quarter. Moreover, household consumption contributed 1.1 percentage points towards Q4 growth after subtracting from growth in the previous quarter. Goods (3.0%) and services (1.3%) consumption expanded in Q4 of 2022. Spending on new vehicles, which have benefited from supply-chain improvements, supported strong growth in durables. Non-profit institutions and governments also contributed marginally to growth in Q4.

Meanwhile, the continued decline in business investment and housing subtracted 1.0 and 0.7 percentage points, respectively, from growth in Q4 of 2022. As higher interest rates take hold, a decrease in both new construction and renovations contributed to the contraction in housing investment. On balance, final domestic demand was weak in the fourth quarter of 2022, increasing by 1.0%.

Source: Statistics Canada Table 36-10-0104-01, retrieved on 2023-03-10.

Text version

| Q3 2021 | Q4 2021 | Q1 2022 | Q2 2022 | Q3 2022 | Q4 2022 | |

|---|---|---|---|---|---|---|

| GDP growth (%) | 5.8 | 6.9 | 2.4 | 3.6 | 2.3 | 0.0 |

| Consumption (percentage points contribution) | 10.8 | 1.4 | 1.7 | 4.3 | 0.8 | 1.6 |

| Investment (percentage points contribution) | -3.5 | 2.3 | 1.3 | -2.2 | -1.6 | -0.6 |

| Inventories (percentage points contribution) | -3.3 | 4.2 | 2.2 | 7.1 | -1.0 | -5.6 |

| Net Trade (percentage points contribution) | 2.1 | -1.1 | -3.0 | -5.8 | 4.1 | 4.7 |

Goods industries contract in q4 as services industries edge up

Real GDP by industry eked forward 0.2% in Q4, as goods-producing industries contracted 0.6% while services industries expanded 0.5%. This constitutes the slowest pace of real GDP growth since the second quarter of 2021.

Following a record quarter, mining, oil and gas extraction decreased by 2.6% in Q4 of 2022, leading the overall contraction in goods. The industry was hit by the continued decline in prices, as well as unexpected supply-chain issues and maintenance needs in December. A 0.7% decrease in manufacturing, driven by decreases in machinery and plastics products manufacturing, also contributed to the overall decline in goods in Q4.

Public administration and health care expanded for the tenth consecutive quarter. Due to the size of the sector, public administration was the largest contributor to growth in the fourth quarter, advancing 1.5% driven in part by municipal elections and a rebound from a decline in September. Health care and social assistance, another large sector, was the second largest contributor to Q4 growth, increasing by 1.2%. Despite bad weather in December, transportation and warehousing activity expanded by 1.6% in Q4 of 2022 as nearly all COVID-19-related travel restrictions were lifted in October.

Source: Statistics Canada Table 36-10-0449-01. Retrieved 2023-03-09.

Text version

| Quarterly % GDP growth in Q4 | |

|---|---|

| Mining, quarrying, & oil & gas extraction | -2.6 |

| Utilities | -0.8 |

| Manufacturing | -0.7 |

| Accommodation & food services | -0.5 |

| Retail trade | -0.3 |

| Information & cultural industries | -0.1 |

| Finance & insurance | -0.1 |

| Real estate & rental & leasing | 0.0 |

| Administrative & waste management | 0.1 |

| All industries | 0.2 |

| Educational services | 0.4 |

| Wholesale trade | 0.4 |

| Other services (except public administration) | 0.5 |

| Construction | 0.8 |

| Professional, scientific & technical services | 1.0 |

| Health care & social assistance | 1.2 |

| Agriculture, forestry, fishing & hunting | 1.3 |

| Public administration | 1.5 |

| Transportation & warehousing | 1.6 |

| Arts, entertainment & recreation | 3.9 |

Services exports remain robust as goods exports continue to decline in Q4

The value of goods and services exports declined for the second consecutive quarter, contracting 1.0% in Q4 of 2022. Goods exports contracted by 2.0%, while service exports expanded by a robust 3.9%. Despite a contraction in the value of exports, export volumes expanded in Q4. The value of goods and services imports contracted for the first time since the start of the pandemic, decreasing by 1.2% in Q4 solely driven by goods (-1.7%), as services imports expanded modestly (0.9%). With imports contracting faster than exports, Canada’s goods and services deficit narrowed to $2.8 billion in Q4 from $3.2 billion in Q3.

Six of 11 goods export product categories contracted in Q4. Strong growth in agriculture (21.4%) and consumer goods (6.7%) exports partially outweighed large contractions in energy (-13.5%) and metal and non-metallic minerals (-5.3%) exports. The continued decline in energy prices and unplanned maintenance and supply-chain issues in December resulted in energy exports being the biggest contributor to the Q4 export contraction. On the services side, a 9.5% increase in Q4 travel services exports reflects the continued recovery in the industry from the start of the pandemic. Commercial services exports expanded by 2.8% in Q4 following a 0.2% contraction in Q3. A modest 0.9% increase in transportation exports also supported growth, while government services exports contracted by 0.8% in Q4.

The contraction in goods imports was widespread, with decreases in 9 of 11 goods categories. Significant declines in consumer goods (-3.8%, driven by declines in pharmaceutical products), chemical and plastic products (-5.0%), and electronic and electrical machinery (-3.1%) led the Q4 contraction. Meanwhile, strength in travel (3.6%) and commercial (0.9%) services imports outweighed Q4 contractions in transportation (-2.0%, partially due to large decreases in marine transport) and government (-0.5%) services imports.

Sources: Statistics Canada Table 36-10-0019-01 & Table 36-10-0021-01. Balance of payments basis, seasonally adjusted.

Text version

| Quarterly % growth in Q4 | Exports | Imports |

|---|---|---|

| Farm, fishing & intermediate food products | 21.4 | -0.3 |

| Aircraft & parts | 12.0 | -3.0 |

| Travel | 9.5 | 3.6 |

| Consumer goods | 6.7 | -3.8 |

| Industrial machinery, equipment & parts | 4.3 | 2.2 |

| Electronic & electrical equipment & parts | 3.3 | -3.1 |

| Commercial services | 2.8 | 0.9 |

| Transportation | 0.9 | -2.0 |

| Motor vehicles & parts | -0.2 | 1.2 |

| Government services | -0.8 | -0.5 |

| Total Goods & Services | -1.0 | -1.2 |

| Chemical, plastic & rubber products | -2.1 | -5.0 |

| Forestry & building & packaging materials | -4.7 | -1.7 |

| Metal ores & non-metallic minerals | -5.3 | -4.4 |

| Metal & non-metallic mineral products | -5.3 | -2.1 |

| Energy products | -13.5 | -2.2 |

Goods exports to the U.S. led the Q4 contraction

Canadian goods exports and imports contracted 2.0% and 1.7%, respectively, in Q4 of 2022. With exports contracting more than imports, Canada’s trade surplus shrank to $1.7 billion in Q4 from $2.5 billion in Q3.

Goods exports to the U.S. (-3.6%) led the Q4 contraction, decreasing for the second consecutive quarter on lower energy exports. Significant increases in new vehicle exports to the U.S. only partially offset decreases elsewhere. A decrease in exports to Hong Kong (-58.7%), primarily of gold, also contributed to the contraction. Altogether, exports outside the U.S. advanced 3.1%, led by goods exports to China, which jumped 20.2% in Q4 on higher oilseeds and wheat exports. Fourth quarter oilseeds and aircraft and parts exports drove the seventh consecutive quarterly increase in goods exports to the European Union (EU; 5.8%).

The contraction in goods imports was widespread across Canada’s major partners, with significant contractions in China (10.4%), the EU (3.9%), and the U.S. (0.7%).

Overall, 2022 was another strong year for Canadian goods trade, with exports and imports reaching new records. However, the contraction in fourth-quarter trade may reflect a trend towards slower growth. Trade is forecasted to slow in 2023 as the global and Canadian economies begin to adjust to higher interest rates and other challenges constraining growth.

Source: Statistics Canada Table 36-10-0023-01, balance of payments basis, seasonally adjusted. European Union does not include the United Kingdom.

Text version

| Quarterly % growth in Q4 | Exports | Imports |

|---|---|---|

| United States | -3.6 | -0.7 |

| China | 20.2 | -10.4 |

| European Union | 5.8 | -3.9 |

| Rest of the world | -1.9 | 0.6 |

Services trade continues to recover

Services trade continued its recovery from the pandemic, with exports and imports recording their tenth consecutive quarterly increase. Services exports advanced 3.9% in Q4 of 2022 while imports edged forward 0.9%, resulting in a narrower services trade deficit at $4.5 billion in Q4 from $5.6 billion in Q3.

Canada’s services exports increased to nearly all major trading partners, with the notable exception of China, where exports contracted 4.5% in Q4 of 2022. Export growth was led by the U.S., which increased by 4.2% in Q4. Services exports to the EU also supported growth, increasing 5.9% in Q4.

Services imports from the U.S. increased 2.6% in Q4 of 2022, following a 7.4% increase in Q3. However, services imports from non-U.S. countries decreased by 1.4% in Q4 – the first quarterly decrease since the early days of the pandemic (Q3 2020). The decrease in service imports was led by contractions in Asia, with notable declines with Hong Kong (8.7%) and China (-5.3%). Service imports from the EU partially offset these declines, advancing 3.1% in Q4 of 2022.

Travel services, the second largest services category, continued their recovery in Q4 of 2022; increased visitor spending drove the 9.5% advance in Q4 exports, as the number of travellers from the U.S. (-0.2%) and non-U.S. destinations (-15.2%) decreased. Meanwhile, travel imports (i.e., Canadians travelling abroad) increased by 3.6%, fuelled by Canadians travelling to the U.S. (11.2%) as travel to non-U.S. destinations decreased (19.4%). While overall services trade has recovered from the impacts of the COVID-19 pandemic, travel services exports and imports remain 5.8% and 20.2% below their Q4 2019 levels, respectively.

Source: Statistics Canada Table 12-10-0157-01, balance of payments basis, seasonally adjusted. European Union does not include the United Kingdom.

Text version

| Quarterly % growth in Q4 | Exports | Imports |

|---|---|---|

| United States | 4.2 | 2.6 |

| China | -4.5 | -5.3 |

| European Union | 5.9 | 3.1 |

| Rest of the world | 4.2 | -3.0 |

Weak domestic demand and a contraction in inventories to slow Canadian growth in 2023

As recovery from the shocks of the global pandemic continued, the Canadian economy expanded by a robust 3.6% in 2022. According to the Bank of Canada’s January 2023 Monetary Policy Report, economic growth is expected to slow to 1.0% in 2023, up slightly from 0.9% in their October 2022 report.

High inflation and tight financial conditions continue to be the drivers of the expected slowdown, with a slight easing of inflation motivating the modest upward revision in the 2023 outlook. Canada’s consumer price index (CPI) peaked at 8.1% in June 2022 and has since come down to 5.9% in January 2023. While an improvement, this is still higher than the Bank of Canada’s 1%-3% inflation target range. The Bank of Canada expects inflation to slow throughout the year, averaging 3.0% in 2023 before falling to 2.0% in 2024.

Modest gains in exports, consumption and government spending will support growth in 2023. While interest rate-sensitive sectors, including housing and investment will drag down growth. Finally, businesses drawing down their inventories will be the biggest factor dragging down growth in 2023. Altogether, the Bank of Canada estimates that it is possible that the Canadian economy avoids a recession or enters a shallow one in 2023. Meanwhile, Oxford Economics, a private sector forecaster, puts the likelihood of a recession occurring in Canada much higher. Oxford Economics forecasts economic growth to contract by 1.3% in 2023, caused by a harsher expected slowdown in the housing market and consumption.

Assuming the Bank of Canada is able to hold the policy rate at 4.5% and inflation eases by the end of 2023, it forecasts economic growth will be 1.8% in 2024. A key risk to this outlook is what happens in the U.S. economy and how far the Federal Reserve raises interest rates.

Source: Bank of Canada, Monetary Policy Report, January 2023.

Text version

| 2022 | 2023 | 2024 | |

|---|---|---|---|

| Canadian forecasted GDP growth (%) | 3.6% | 1.0% | 1.8% |

Special focus on labour markets

Labour markets remain a wildcard

The Canadian labour market ended 2022 strong – with unemployment averaging 5.1%, close to historic lows, job vacancies (i.e., unmet demand for labour) remaining elevated, and the participation rate edged up to 65.4% (somewhat lower than pre-pandemic but still strong) in Q4. This strength continued as the new year kicked off. The unemployment rate barely budged, coming in at 5.0% in February of 2023, while more jobs were added to the economy, and the participation rate nudged upward.

The labour market barrelled forward after the initial shock of the COVID-19 pandemic in the summer of 2020. One of the positive stories from this rebound has been a shift in female workers into higher-paying jobs. Women moved from high-contact jobs, such as those in health care, to low-contact jobs, such as those in finance, which also tend to be higher paying.

Gender dynamics aside, the labour market is somewhat of a wildcard for the Canadian economic outlook. As strength in the labour market continues, the spending power of Canadians is reinforced and is seen as a sign of excess demand by the Bank of Canada. Ultimately, tight labour markets potentially make the Bank of Canada’s goal of taming inflation harder to achieve.

It may not be intuitive to hear forecasters calling for a recession at the same time that labour markets are historically tight. The reason for this is, in large part, because interest rates climbed significantly in 2022, but they impact the economy at a lag. Hence, many forecasters argue that the Canadian economy is in excess demand and that interest rate hikes and weak global demand will take the wind out of its sales soon enough. At that point, it would likely be reflected in the labour market, with an expected slowdown in job growth or potentially job losses.

Source: Statistics Canada Table: 14-10-0287-01 & Table: 14-10-0406-01.

Text version

| Canadian Unemployment and Job Vacancies | Unemployment Rate (%, seasonally adjusted) | Job Vacancies (thousands of jobs, seasonally adjusted) | |

|---|---|---|---|

| Oct-20 | 9.0 | 573.1 | |

| Nov-20 | 8.7 | 567.145 | |

| Dec-20 | 8.9 | 562.415 | |

| Jan-21 | 9.2 | 564.865 | |

| Feb-21 | 8.5 | 615.88 | |

| Mar-21 | 7.6 | 640.73 | |

| Apr-21 | 8.2 | 649.555 | |

| May-21 | 8.2 | 671.01 | |

| Jun-21 | 7.8 | 766.485 | |

| Jul-21 | 7.5 | 819.555 | |

| Aug-21 | 7.2 | 888.19 | |

| Sep-21 | 7.1 | 922.445 | |

| Oct-21 | 6.6 | 918.17 | |

| Nov-21 | 6.2 | 909.995 | |

| Dec-21 | 6 | 963.775 | |

| Jan-22 | 6.5 | 926.725 | |

| Feb-22 | 5.4 | 917.92 | |

| Mar-22 | 5.3 | 986.155 | |

| Apr-22 | 5.3 | 992.545 | |

| May-22 | 5.2 | 1002.175 | |

| Jun-22 | 4.9 | 981.585 | |

| Jul-22 | 4.9 | 968.63 | |

| Aug-22 | 5.3 | 920.865 | |

| Sep-22 | 5.2 | 907.655 | |

| Oct-22 | 5.2 | 870.795 | |

| Nov-22 | 5.1 | 849.175 | |

| Dec-22 | 5 | 848.815 | |

| Jan-23 | 5 | ||

| Feb-23 | 5 |

Annex: Tables

Table 1: Canadian trade by industry sector ($ millions)

| Exports | Imports | |||||

|---|---|---|---|---|---|---|

| Q4 – 2022 | Q/Q % | Y/Y % | Q4 - 2022 | Q/Q % | Y/Y % | |

| Goods | 193,894 | -2.0 | 22.3 | 192,222 | -1.7 | 19.8 |

| Resource products | 118,232 | -5.6 | 28.8 | 65,697 | -2.8 | 24.8 |

| Energy products | 47,816 | -13.5 | 56.8 | 13,006 | -2.2 | 58.3 |

| Non-resource products | 70,435 | 4.3 | 12.9 | 119,222 | -1.2 | 17.6 |

| Industrial machinery & equipment | 12,052 | 4.3 | 19.0 | 22,804 | 2.2 | 23.9 |

| Electronic machinery & equipment | 8,350 | 3.3 | 17.8 | 21,149 | -3.1 | 14.0 |

| Motor vehicles and parts | 20,410 | -0.2 | 12.5 | 30,495 | 1.2 | 19.9 |

| Aircraft & other transportation equipment | 7,095 | 12.0 | 1.8 | 6,080 | -3.0 | 19.0 |

| Consumer goods | 22,528 | 6.7 | 11.9 | 38,694 | -3.8 | 14.5 |

| Services | 42,335 | 3.9 | 15.1 | 46,788 | 0.9 | 22.4 |

| Travel | 9,175 | 9.5 | 72.6 | 9,980 | 3.6 | 221.4 |

| Transportation | 5,008 | 0.9 | 27.6 | 8,883 | -2.0 | 31.6 |

| Commercial | 27,786 | 2.8 | 3.6 | 27,490 | 0.9 | 1.9 |

| Government | 366 | -0.8 | 4.4 | 435 | -0.5 | 3.1 |

| Total Goods and Services | 236,229 | -1.0 | 21.0 | 239,010 | -1.2 | 20.3 |

Note: “Q/Q %” is the change from the previous quarter; “Y/Y %” is yearly change.

Source: Statistics Canada Table 36-10-0019-01 & 36-10-0021-01. Balance of payments basis, seasonally adjusted.

Table 2: Canadian goods trade by trading partner ($ millions)

| Exports | Imports | |||||

|---|---|---|---|---|---|---|

| Q4 – 2022 | Q/Q % | YTD % | Q4 – 2022 | Q/Q % | YTD % | |

| United States | 145,453 | -3.6 | 0.2 | 121,205 | -0.7 | 0.2 |

| Mexico | 2,632 | 10.6 | 0.1 | 6,120 | -5.2 | 0.2 |

| European Union | 9,787 | 5.8 | 0.2 | 17,323 | -3.9 | 0.2 |

| France | 1,056 | 4.6 | 0.0 | 1,476 | -0.3 | 0.1 |

| Germany | 1,928 | -9.7 | 0.1 | 4,937 | 0.8 | 0.2 |

| United Kingdom | 4,117 | -14.3 | 0.1 | 2,317 | 4.4 | 0.0 |

| India | 1,948 | 66.1 | 0.8 | 1,688 | -1.7 | 0.4 |

| China | 8,934 | 20.2 | 0.0 | 16,328 | -10.4 | 0.2 |

| Japan | 4,398 | -2.2 | 0.2 | 3,007 | -4.8 | 0.1 |

| South Korea | 1,896 | -9.9 | 0.4 | 2,675 | -1.6 | 0.3 |

| Rest of the world | 14,729 | -3.9 | 0.1 | 21,559 | 3.3 | 0.2 |

| Total Goods Trade | 193,894 | -2.0 | 0.2 | 192,222 | -1.7 | 0.2 |

Note: “Q/Q %” is the change from the previous quarter; “Y/Y %” is yearly change.

Source: Statistics Canada Table 36-10-0023-01. Balance of payments basis, seasonally adjusted.

Table 3: Canadian services trade by trading partner ($ millions)

| Exports | Imports | |||||

|---|---|---|---|---|---|---|

| Q4 – 2022 | Q/Q % | YTD % | Q4 – 2022 | Q/Q % | YTD % | |

| United States | 22,837 | 4.2 | 11.8 | 27,072 | 2.6 | 21.7 |

| Mexico | 503 | 10.3 | 26.6 | 727 | 12.4 | 72.1 |

| European Union | 4,955 | 5.9 | 13.9 | 5,855 | 3.1 | 18.4 |

| France | 1,206 | 3.9 | 23.1 | 969 | 6.5 | 28.8 |

| Germany | 860 | 11.0 | 3.6 | 1,045 | 3.6 | 17.5 |

| United Kingdom | 2,035 | 6.3 | 13.0 | 2,413 | 2.1 | 16.2 |

| India | 1,611 | -0.4 | 22.7 | 761 | 1.9 | 19.4 |

| China | 1,942 | -4.5 | 34.1 | 1,043 | -5.3 | 26.7 |

| Japan | 533 | 6.8 | 21.7 | 803 | -2.3 | 37.3 |

| South Korea | 392 | 3.4 | 34.2 | 159 | 5.3 | 33.0 |

| Rest of the world | 7,527 | 4.2 | 19.4 | 7,955 | -6.2 | 24.7 |

| Total Services Trade | 42,335 | 3.9 | 15.1 | 46,788 | 0.9 | 22.4 |

Note: “Q/Q %” is the change from the previous quarter; “Y/Y %” is yearly change.

Source: Statistics Canada, Table 12-10-0157-01. Balance of payments basis, seasonally unadjusted.

- Date modified: